Results‑based financing (RBF) has become one of the most widely used instruments in development and climate finance. Across energy access, clean cooking, health, and education, it has been deployed to link concessional capital more directly to measurable outcomes. In Nigeria’s energy sector in particular, RBF has played a meaningful role in expanding access, accelerating private‑sector delivery, and improving accountability.

Yet as the energy transition accelerates, an increasingly important question is emerging: can RBF support not just market expansion, but a sustainable market transition?

This question is especially pressing in contexts dominated by entrenched fossil‑fuel technologies – where the challenge is no longer first‑time access, but the displacement of assets that are cheap, familiar, accessible, and repeatedly replaced.

Nigeria’s fossil‑fuel generator market provides an illustration of this different challenge.

Nigeria’s generator economy – a transition challenge, not an access gap

Nigeria has one of the largest generator markets in the world. Fossil‑fuel generators are deeply embedded across households, SMEs, commercial facilities, and public institutions, driven by chronic grid unreliability. For many users, generators are not just a backup option but their primary energy asset.

While diesel and petrol generators are expensive to run and highly polluting, they persist because they solve a real problem – reliable power.

Solar‑battery generator systems are now technically mature and increasingly competitive on lifetime cost. For many use cases, they already offer lower operating costs, quieter operation, and significant health and environmental benefits. The core barrier to adoption is not technology, but upfront affordability and perceived risk at the point of purchase.

This is why RBF is a relevant instrument in the Nigerian context. Unlike credit lines or concessional debt – which improve capital availability upstream but often fail to shift retail prices – RBF operates at the point of market decision, where buyers compare upfront cost, perceived risk, and familiarity.

However, applying standard RBF templates to generator replacement raises new challenges.

Why “business‑as‑usual” RBF falls short in generator markets

Nigeria is not new to RBF. Programmes such as the Nigeria Electrification Project, the Universal Energy Facility, and DARES demonstrate that RBF can be implemented at scale, deployed with new innovations, and integrated into complex delivery ecosystems.

The critique here is therefore not a rejection of RBF, nor a dismissal of Nigeria’s experience. Rather, it reflects a shift in the problem being addressed.

Most RBFs in the energy sector were designed to start and scale new markets, particularly to expand first‑time access. Generator replacement, by contrast, is a market‑transition challenge. It requires sustained behavioural change, asset substitution, and confidence that clean alternatives can fully replace an incumbent technology.

In this context, standard RBF designs tend to fall short in predictable ways:

- They reward deployment, not displacement – Paying for systems sold or installed does not guarantee that fossil generators are retired or meaningfully displaced. In many cases, solar systems are stacked alongside generators rather than displacing them. This is reinforced by monitoring and verification (M&V) frameworks that confirm installation but do not track usage or reduced generator runtime. As a result, stacked and displaced systems appear identical in verification terms, making genuine transition effectively invisible to the incentive mechanism.

- They assume firms can pre‑finance delivery – Post‑hoc reimbursement models place significant working‑capital stress on distributors, favouring larger firms with stronger balance sheets and excluding many local players well-positioned to serve SMEs.

- They struggle to adapt to fast‑evolving markets – Fixed targets and static incentive structures can quickly become misaligned with changing technology costs, business models, and customer behaviour.

- They clash with service‑based business models – Many solar generator deployments rely on energy‑as‑a‑service or PAYGo models, where revenues accrue gradually through customer payments over time. Standard RBFs, which trigger payments on upfront sales or installations, are poorly aligned with these cash‑flow profiles. Post‑hoc verification and lump‑sum disbursements can exacerbate working‑capital strain, front‑load risk onto distributors, and amplify portfolio‑at‑risk in PAYGo models – undermining the very business models intended to improve affordability and reliability.

- They lock in short time horizons – Short verification cycles prioritise speed over durability, discouraging investment in system sizing, after‑sales support, and long‑term performance.

- They treat sustainability as something that happens later – Many RBFs compress prices temporarily without strengthening distributor bankability, lender confidence, or customer financing pathways. This leads to market reversion once subsidies end.

For generator replacement, these failures are particularly acute. Poorly designed incentives risk creating short‑term sales spikes while undermining trust in solar generators as a reliable, credible alternative.

From optimisation to redesign – what a “next‑generation” RBF would look like

Much recent RBF innovation has focused on optimisation: digitising M&V, automating payments, or reducing administrative costs. These improvements matter, but they do not resolve the deeper design tensions described above.

What is needed instead is a redesign of RBF as a market‑shaping instrument, deliberately aligned with transition objectives.

In generator markets, this implies several structural shifts:

- From deployment metrics to displacement‑oriented outcomes, rewarding sustained substitution rather than one‑off installations.

- From post‑hoc reimbursement to liquidity‑aware incentives, reducing working‑capital stress through staged payments or complementary liquidity mechanisms.

- From short‑term outputs to time‑weighted performance, recognising that behavioural replacement unfolds gradually.

- From temporary price support to durable market conditioning, using incentives to improve firm bankability, lender confidence, and financing pathways over time.

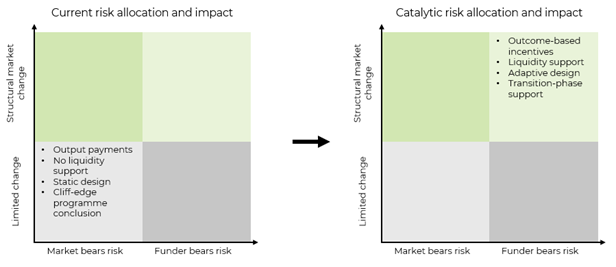

Taken together, these shifts imply a different understanding of risk in RBF design. Rather than minimising exposure by default, an action which may protect the funder, but also often constrains who can participate and how the market evolves. A transition‑oriented RBF asks which uncertainties must be absorbed by the programme in order to unlock durable market behaviour – and which can realistically be left with market actors.

The figure below reframes these design shifts through a risk‑allocation lens, illustrating how absorbing specific market risks enables specific transition behaviours.

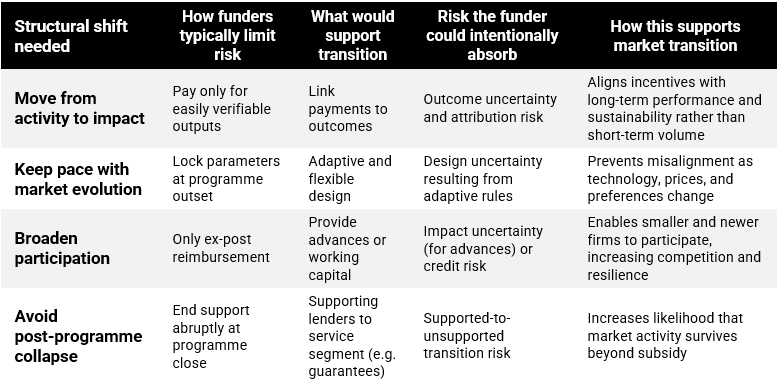

Figure 1. Simplified illustration of how risks can be reallocated to achieve specific goals

- Absorbing outcome uncertainty, to incentivise long‑term performance – Moving from easily verifiable outputs to higher‑order outcomes increases uncertainty for the funder, as outcomes are harder to observe, attribute, and measure with precision. However, by accepting this loss of simplified certainty, the funder enables incentives that pull market actors toward behaviours consistent with long‑term sustainability rather than short‑term optimisation. In other words, absorbing outcome uncertainty is what allows the programme to reward what ultimately matters, rather than what is easiest to count.

- Absorbing design uncertainty, to enable adaptive market alignment – Locking in RBF parameters at the outset creates a tightly controlled risk environment for funders, placing emphasis solely on execution, but assumes that markets, technologies, and customer preferences will remain stable over time. By allowing for adaptive design – adjusting parameters over time in response to market signals – funders accept greater uncertainty and open‑ended risk. In return, they reduce the risk borne by market actors of being locked into misaligned criteria, and increase the likelihood that the RBF remains relevant as conditions evolve.

- Absorbing liquidity and balance sheet risk, to broaden market participation – Restricting RBF payments to ex‑post reimbursement shifts liquidity and credit risk onto participants, effectively limiting participation to firms with strong balance sheets. This skews incentives toward incumbents and inhibits broad‑based market formation. By contrast, mechanisms such as advance payments, working‑capital facilities, or forgivable loans deliberately absorb some liquidity and credit risk. While this increases exposure for the funder, it performs a clear function: enabling participation by smaller or newer firms and supporting a more distributed and competitive market structure.

- Absorbing transition-phase risk, to secure post-programme viability – Treating post‑programme market viability as external to the RBF places the full burden of transition‑phase risk on market actors, who must achieve sustainability before support ends or face a cliff edge. An alternative approach is for funders to absorb some of this risk – for example by offering temporary risk guarantees to lenders serving the segment. This does not eliminate commercial discipline, but it buys time for markets to stabilise and for private capital to step in. Absorbing transition‑phase risk in this way directly increases the probability that programme‑induced activity survives beyond the subsidy period.

Why Nigeria is an ideal test case

Nigeria is not a fragile or speculative environment for this kind of experimentation. On the contrary, it offers a rare combination of:

- A large, economically significant generator market

- A commercially active solar ecosystem

- Institutions experienced in implementing RBFs

- A proven track record of RBF delivery, and innovation, at scale

This reduces execution risk and allows a pilot to focus squarely on design questions rather than basic feasibility. At the same time, Nigeria’s deeply entrenched generator economy provides a deliberately demanding test – if a redesigned RBF can support meaningful displacement here, the lessons will be widely applicable.

Importantly, the relevance of such a pilot would extend beyond generators. Many other sectors – clean cooking, productive‑use appliances, decentralised cooling, and e‑mobility – face similar dynamics: incumbent technologies that are cheap and familiar, cleaner alternatives that are cost‑effective over time but unaffordable upfront, fragmented demand, and financial systems hesitant to support.

Looking ahead

RBF remains an attractive instrument because it promises accountability and alignment between funding and real‑world outcomes. But experience across energy access and adjacent sectors shows that how RBF is designed matters as much as whether it is used at all.

There is now an opportunity to evolve RBF from a tool optimised for market expansion into one capable of supporting market transition. Nigeria’s generator economy offers a compelling place to do so – addressing an urgent energy challenge while contributing evidence to the broader reform agenda.

We are now looking to progress this work from diagnosis to demonstration, including developing and piloting a redesigned RBF for generator replacement in Nigeria.

If you are a funder, RBF practitioner, or solar generator distributor active in the Nigerian market and interested in shaping the next generation of RBF, we would welcome the opportunity to engage as we develop our concept note of what this could look like. Further information is available at ZE‑Gen.org, and our white paper expanding on the above discussion in more detail will be published shortly.

Addendum: Linking risk allocation to market transition